Non-GamStop Slots: The UK Operator Landscape, Licensing Reality & Player Data

Offshore slot data without the marketing gloss.

The Offshore Slot Market UK Players Actually See

I open the same monitoring panel every weekday morning — a list of roughly seven hundred offshore operators that target UK players, each scraped overnight for fresh bonus pages, payment rails and licence references. After nine years of watching this segment, the pattern is stable: the phrase "not on GamStop" sits in the headline of more offshore landing pages aimed at British residents than any other slogan in the niche.

This article maps that segment as a market, not as a route to a deposit page. Two terms anchor everything that follows.

GAMSTOP — the national online self-exclusion register operated by GAMSTOP Group, a non-profit funded by the UK gambling industry. Every operator holding a UKGC remote licence must integrate with the register and block any UK resident enrolled on it.

UKGC — the UK Gambling Commission, the statutory regulator for commercial gambling in Great Britain. It licenses operators, sets technical and consumer-protection rules, and enforces against unlicensed activity aimed at UK consumers.

The moment a UK resident signs themselves onto the GAMSTOP database, every UKGC-licensed online slot site refuses their account. Sites that operate without a UKGC licence sit outside that perimeter — they do not query the register, so a self-excluded player can register and deposit anywhere. This is the entire loophole the "non-GamStop" segment turns on.

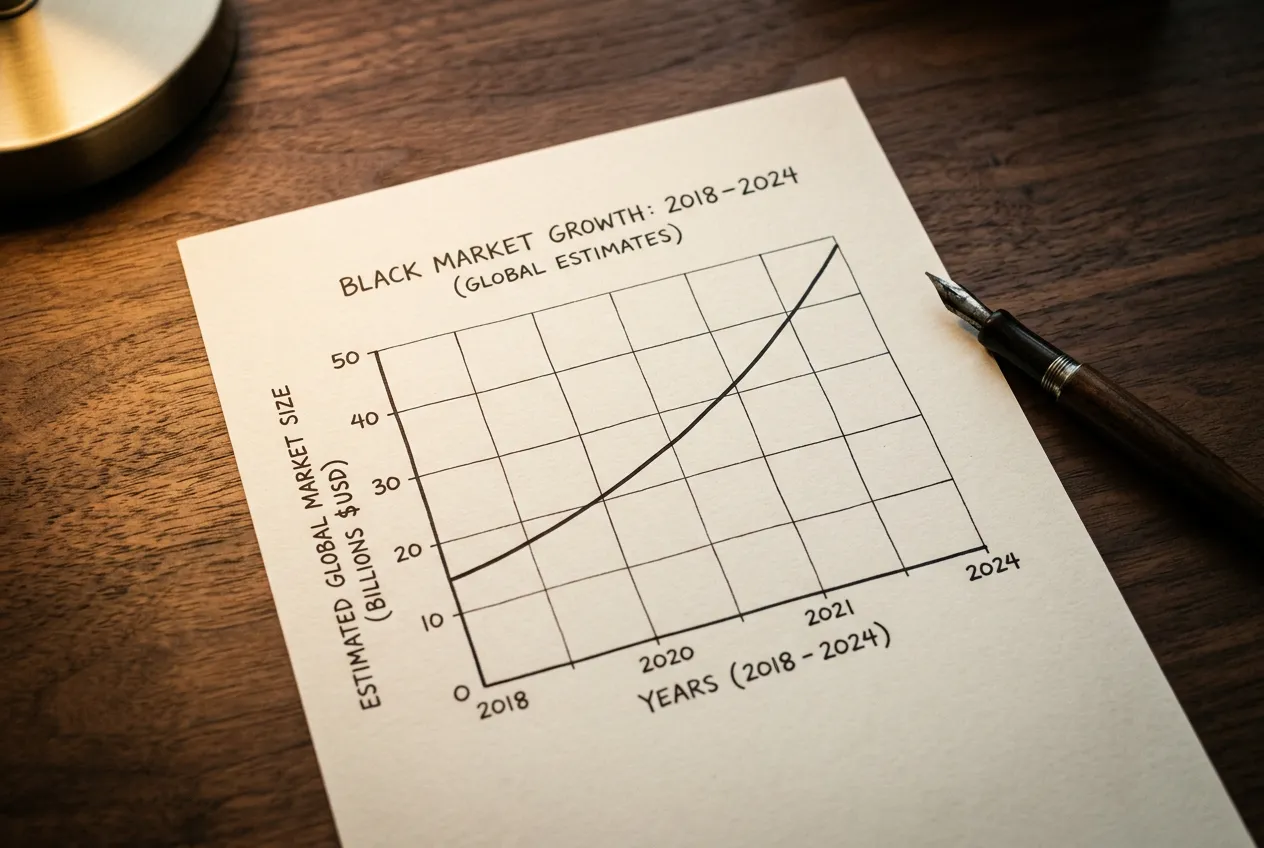

The scale is no longer fringe. The UK black market for online gambling has gone from 0.43 per cent of all wagering activity in 2020 to roughly nine per cent by 2025, and 84 per cent of all promotional activity by unlicensed operators in the UK now centres on the "not-on-GamStop" framing. The offshore slot ecosystem now spends most of its UK marketing budget arguing that self-exclusion is something to step around. What follows walks through the licensing map, the legal status of access from the UK, the financial scale of the unlicensed share, the stake-cap trigger of the latest migration wave, the bonus and payment architecture, and the protections a player loses at the perimeter.

The Eight-Minute Briefing

- 562,000 UK residents sit on the GAMSTOP register at end of 2025; offshore operators that ignore that register form the entire "non-GamStop" segment.

- The unlicensed share of UK gambling has reached roughly 9%, with annual wagering at these sites estimated at £16.6 billion in 2025 — more than triple 2019.

- The £5 spin cap, and the £2 cap for 18–24-year-olds introduced in 2025, is the most direct trigger of offshore migration visible in current data.

- Non-GamStop operators sit outside UKGC rules: no IBAS dispute route, no 10× wagering cap, no FSCS cover on player funds. The trade-off is structural, not cosmetic.

Non-GamStop Slots at a Glance: Numbers That Frame the Niche

The most counterintuitive thing about this market is that the numbers are not estimates. The UKGC publishes quarterly slot GGY to the nearest million; GAMSTOP releases half-year reports with new-registration counts down to the hundred; Yield Sec sizes unlicensed activity from observable promo and traffic data. So the niche can be seen clearly. Here is the frame.

GAMSTOP registrants

562,000 by end of 2025; 58,675 new in H2 alone — about 319 a day.

UK unlicensed share

~9% of total wagering activity in 2025, up from 0.43% in 2020.

UK wagering at unlicensed sites

£16.6 billion in 2025 by H2 Gambling Capital — more than 3× the 2019 figure.

Typical wagering at offshore venues

35–45× on welcome offers, against the UKGC 10× cap that took effect in December 2025.

UKGC spin cap

£5 from 9 April 2025 for all adults; £2 from 21 May 2025 for 18–24-year-olds.

Remote Gaming Duty

40% from April 2026 — a structural cost the offshore segment does not pay.

A regulated and an unregulated slot market sit alongside each other in the UK, and the unregulated one keeps gaining share even as the licensed market grows. The duty hike to 40% from April 2026 will widen the cost gap between the two sides further — a UKGC-licensed operator now pays nearly half of remote GGY in tax while an offshore site licensed in Anjouan or Curaçao pays nothing comparable. The structural pressure on both sides of the perimeter is moving in opposite directions.

By every metric the public regulator publishes, the licensed slot market is growing. By every metric the independent analysts publish, the unlicensed one is growing faster. The pillar between them — self-exclusion enforced through GAMSTOP — is what separates an "operator" from a "non-GamStop operator" in the strict sense.

What “Non-GamStop Slots” Actually Means

Two ideas hide inside the phrase. Most player-facing content collapses them into one. The first is operational — a slot site that does not check the GAMSTOP register. The second is regulatory — a slot site that holds no UKGC licence at all. The two overlap completely in practice, but it helps to keep them apart.

DEFINITION

A non-GamStop slot site is an online casino offering slot games that does not check the UK national self-exclusion register before allowing a UK resident to sign up. In every documented case I have audited, the operator achieves this by holding a licence other than UKGC — usually Curaçao, Anjouan, MGA or Costa Rica — which carries no requirement to integrate with GAMSTOP.

RTP — Return to Player. The long-run percentage of total wagered amounts that a slot returns to players in winnings, averaged over millions of spins. A 96 per cent RTP slot keeps £4 of every £100 wagered, on average. RTP describes a long-tail mathematical expectation, not the outcome of any individual session.

GGY — Gross Gambling Yield. The amount operators keep after paying out winnings — total wagers minus total returns. It is the UK regulator's preferred unit for sizing the market and the figure the 40 per cent Remote Gaming Duty applies to from April 2026.

The term exists because GAMSTOP has reach. The register held 562,000 enrolled UK residents at the end of 2025, and the Ipsos study commissioned by GAMSTOP found that 75 per cent of those users no longer played online at all. The remaining 25 per cent are the audience the unlicensed segment specifically targets, and Yield Sec's analysis of UK-facing offshore promo puts the share aimed at this group above any other lifestyle segment.

Practically, "non-GamStop slots" today means a game library on a platform licensed outside the UK, accepting UK debit cards or crypto without checking GAMSTOP, running software that may include features (bonus buys, configurable RTP profiles, max-stake spins) not permitted on UKGC-regulated sites. The software is often the same. The wrapper is different. The mechanics of RTP-weighted game selection across these venues sit in their own dedicated cluster.

The GAMSTOP Scheme: Scale, Demographics, Auto-Renewal

Every February, GAMSTOP releases the H2 report from the previous calendar year, and it has become my second-most-cited document after the UKGC quarterly market data. It is the only place in the entire UK gambling stack where you can see who is opting out, for how long, and at what age. That visibility is also why the offshore market reads it as closely as the regulator does.

The headline figure is now 562,000 cumulative UK residents enrolled by the end of 2025. The half-year alone added 58,675 — an average of 319 new enrolments a day across H2. The growth has not flattened.

The demographic shift is the more important story. Registrations from 16–24-year-olds rose 40 per cent year-on-year in H2 2025, and that age band now accounts for 29 per cent of all new enrolments. There is no clean way to read this other than as a generational shift in who is asking for self-exclusion.

Tenure is where the scheme has matured. 47 per cent of all GAMSTOP enrolees choose the five-year option — the longest available. Among 16–24-year-olds the picture inverts: 38 per cent choose six months, treating self-exclusion as a deliberate timeout. As of December 2025, more than half of the five-year cohort had activated the auto-renewal toggle, locking themselves out for another five years without a manual confirmation step. Fiona Palmer's framing is worth reading in her own words: continued year-on-year growth in registrations highlights the increasing need for effective self-exclusion tools, and the rise in take-up of auto-renewal in particular shows that many consumers are seeking longer-term support.

562,000 enrolled. 47 per cent choose the longest available term. Half of those activate auto-renewal. The "non-GamStop" niche exists because a scheme designed to be hard to escape is, by user choice, getting harder to escape.

From the scheme itself to its legal periphery — what the law actually says about a player who decides to look past it.

Is It Legal to Play Non-GamStop Slots from the UK?

This is the single most asked question in trade conversations I have, by a wide margin, and the answer requires two clean distinctions. The first separates the player from the operator. The second separates legality from protection.

A UK resident playing online slots at a site not licensed by the UKGC is not, in themselves, committing a criminal offence. The Gambling Act 2005 places the licensing obligation on the operator, not on the consumer. So the question "is it illegal for me to deposit at a non-GamStop site?" has a narrow answer of no.

LEGAL

Operating an online gambling business that targets or accepts UK customers without a UKGC remote licence is a criminal offence under section 33 of the Gambling Act 2005. The penalty includes prosecution and unlimited fines. The Act does not criminalise the individual consumer for depositing or wagering at such a site.

The second distinction matters more in practice. Legal does not mean protected. The moment a UK resident funds an account at a non-UKGC site, every consumer-protection layer the UKGC framework provides — alternative dispute resolution, operational rules on withdrawals, GAMSTOP integration, financial vulnerability triggers, the audit of RTP integrity — falls away. The player is not breaking the law. They are operating outside the framework that exists to protect them when something goes wrong.

That distinction matters because the unlicensed market is not benign. UK wagering at unlicensed sites is now estimated at £16.6 billion a year by H2 Gambling Capital — more than triple the 2019 figure. Yield Sec sizes the share of total UK gambling activity captured by these operators at roughly 9 per cent in 2025, up from 0.43 per cent in 2020. Andrew Rhodes, the chief executive of the UKGC, put the regulator's view plainly: the illegal online market is unsafe, unfair and criminal, which is why the Commission has invested heavily in this area in recent years. The criminal element applies to the operator. The "unsafe and unfair" element applies to the player.

RISK NOTICE

The legality question is the wrong filter. A UK resident faces no criminal liability for depositing at a non-UKGC site, but they also have no statutory dispute route if the operator refuses a withdrawal, no FSCS cover on cash held in operator accounts, no GAMSTOP-linked block to enforce a self-exclusion choice, and no audit trail on the RTP or game outcomes.

The Licensing Map: Curaçao, MGA, Anjouan & Beyond

Asked five years ago which licence to look up first on a non-GamStop site, I would have said Curaçao without hesitation and the conversation would have ended there. As of January 2025 that answer is no longer adequate.

The pivot happened on 24 December 2024. The Curaçao National Ordinance on Games of Chance — LOK — came into force, replacing the 1993 Offshore Games Ordinance that had governed the island's regime for thirty-one years. Every sub-licence issued under the old four-master-licence structure was annulled with effect from 31 January 2025; the last master-licence itself expired the same day. Every site that wanted to keep operating from Curaçao had to apply directly to the Curaçao Gaming Authority for a new B2C licence. Annual fees under LOK run to roughly €47,000 for B2C and €24,000 for B2B, with mandatory local presence required from 2028–2029.

| Jurisdiction | Regulator | Indicative annual fees | UK consumer access | Practical strength |

|---|---|---|---|---|

| Malta (MGA) | Malta Gaming Authority | €25,000–€35,000 plus levy | Permitted under MGA terms; no UKGC equivalence | Strongest of the offshore tier — published register, ADR scheme, audited game submissions. |

| Curaçao (post-LOK) | Curaçao Gaming Authority | ~€47,000 B2C | Prohibited in law, rarely enforced in practice | Improving from a low base; verifiable register, ADR mechanisms still maturing. |

| Anjouan | Anjouan Offshore Finance Authority | Lower five-figure range | No explicit UK ban | Light-touch regime; public-register verification limited. |

| Isle of Man (IOM) | Gambling Supervision Commission | £35,000+ | Permitted under IOM terms; no UKGC equivalence | Comparable to MGA in process rigour; smaller operator pool. |

| Costa Rica | None (registered as data-services) | Variable; no formal licence | No specific UK rule | Effectively unlicensed; no regulator to escalate disputes to. |

The Curaçao entry requires a closer reading. LOK as written prohibits Curaçao-licensed operators from accepting players resident in jurisdictions where their activity would breach local law — the UK is exactly that case, because the operator does not hold a UKGC licence. In practice, as of early 2026, visible enforcement of this clause is close to zero. Operators continue to accept UK deposits and quote a Curaçao licence in their footer. The clause exists; the consequence does not, yet.

MGA and IOM sit at the opposite end of the curve. Both regulators publish searchable operator registers, run alternative-dispute-resolution mechanisms with documented timelines, and audit game-output certification through accredited test houses. The cost of holding either reflects that overhead. Anjouan is the wild card — the regime that absorbed the largest share of Curaçao sub-licensees after the LOK reset, partly because the fees are lower and partly because the regulator publishes a register but does not require the same operational disclosure. For a player auditing an operator, an Anjouan licence is harder to verify than an MGA or IOM number.

UKGC vs Non-GamStop: A Side-by-Side Reality Check

This is the comparison most players come to the topic looking for, and most affiliate sites give it as a sales matrix instead of a regulatory one. Sales matrices show what offshore offers more of. Regulatory matrices show what gets removed from the equation in the process. Both are real. Only one of them matters when something goes wrong.

KYC — Know Your Customer. The identity-verification process operators must run to satisfy anti-money-laundering rules and confirm a player is who they say they are. Under UKGC rules, ID verification must happen before a deposit; offshore operators typically defer it to first withdrawal.

FRA — Financial Risk Assessment. The UKGC framework requiring operators to run a financial vulnerability check when a player's net deposits cross a defined threshold. Implemented in stages from August 2024.

| Variable | UKGC-licensed | Non-GamStop (offshore) |

|---|---|---|

| Max spin stake (slots) | £5 from 9 April 2025; £2 for 18–24 from 21 May 2025 | No statutory cap; commonly £100+, occasionally £500 |

| Spin speed | Minimum 2.5-second interval | Turbo spin and autoplay generally permitted |

| Wagering on bonuses | Capped at 10× from 19 December 2025 | Industry norm 35–45×; outliers 60×+ |

| Bonus buys / feature buys | Prohibited at UKGC sites since 2023 | Widely available where the game studio offers them |

| KYC timing | Pre-deposit, mandatory | Typically deferred until first withdrawal |

| Financial vulnerability checks (FRA) | Triggered at £150 net deposit in 30 days (since 28 Feb 2025) | None comparable |

| Self-exclusion register | GAMSTOP integration mandatory | Not integrated |

| Dispute path | IBAS and UKGC complaint route | Whichever ADR the operator nominates, if any |

| RTP transparency | Operator and game RTP must be displayed | Variable; often visible only inside the paytable |

A few rows need unpacking. The £150 FRA trigger gets most overstated in player-facing content — the pilot phase showed 97 per cent of checks pass without the player noticing, running in the background against credit-reference data. The picture sold to offshore-leaning audiences — "the UKGC asks for payslips at £150" — does not survive contact with the pilot data, even though the loudest version of that picture is the one driving the migration conversation.

The 10× wagering cap, in force at UKGC sites since 19 December 2025, is the row that most directly changes the economics. A £100 bonus with 10× wagering needs £1,000 of cycled play to clear; the same bonus at an offshore site with 40× wagering needs £4,000. The bigger headline is usually the worse contract. The spin-stake row is the one most directly responsible for the migration wave Yield Sec has measured through 2025: £5 is a hard ceiling at UKGC sites; offshore operators routinely accept £20, £100, £500 per spin. For a player who structures bankroll around large single spins, the £5 cap is a binding constraint.

UK Online Slot Market & the Unlicensed Share

Sizing the slot market is one of the few areas of UK gambling where the official numbers and the independent numbers agree closely on the licensed side and then diverge wildly on the unlicensed side. That divergence is the whole story of this section.

The licensed picture is clean. UK industry-wide GGY for April 2023 to March 2024 came in at £15.63 billion across all gambling formats. Online slots alone produced £3.6 billion of that over the same period. From Q2 2025–26 onwards the UKGC has published quarterly slot GGY independently: £746.5 million in July–September 2025, £788 million in October–December 2025 on 25.7 billion individual spins, and £773 million in January–March 2026. The trend is consistent: roughly £760–790 million in slot GGY per quarter, no sign of saturation. Andrew Rhodes has put the slots-and-casino combined figure at £4.4 billion for 2023/24 — slots being roughly 60 per cent of the entire UK remote sector once lotteries are stripped out.

The unlicensed picture is where the disagreement starts. Yield Sec, the analytics firm that has tracked the UK illegal market most consistently, puts the unlicensed share at roughly 9 per cent of total wagering activity by 2025 — up from 0.43 per cent in 2020. Its H1 2025 report priced the revenue captured by unlicensed operators at £379 million for the half-year. H2 Gambling Capital, the data house behind Treasury and DCMS modelling, prices annual UK wagering at unlicensed sites at £16.6 billion in 2025, more than triple the 2019 figure.

DATA NOTE

UKGC quarterly slot data is reported as GGY (operator revenue net of player winnings). H2 Gambling Capital's £16.6 billion is wagering activity (gross stake). The two units are not directly comparable; converting between them requires assuming a house edge, which for online slots typically sits at 4–7 per cent of total wagering. The exact GGY of the unlicensed UK market is genuinely contested between Yield Sec, H2 Gambling Capital and BGC internal estimates.

Ismail Vali, the Yield Sec founder with the longest continuous dataset on this segment, summarised the trajectory in late 2025: if you look at Great Britain, it is frightening, because since the firm first talked about this in 2020 it has doubled every year, and now we are at this horrible height. From 0.43 per cent to 9 per cent over five years is a roughly twenty-fold increase — approximately doubling annually, exactly the curve Vali described. The structural reason analysts expect the unlicensed share to keep rising regardless of enforcement is the duty differential: UKGC-licensed operators pay 21 per cent Remote Gaming Duty on UK GGY today, rising to 40 per cent from April 2026. Offshore operators pay no UK gaming duty at all.

£788 million in licensed slot GGY in a single quarter. £16.6 billion in annual wagering at unlicensed sites. 9 per cent of all UK gambling activity outside the regulated perimeter. The licensed market is growing; the unlicensed market is growing faster.

The £5/£2 Stake Caps and What Drives Players Offshore

I called the policy team at one of the larger UKGC-licensed operators the day after the £5 cap took effect in April 2025 and got the same answer I had heard half a dozen times that morning: the top 5 per cent of accounts by stake size had stopped logging in. By July the same accounts had migrated. The £5 cap was not the only trigger of offshore migration in 2025, but it was the most measurable.

The dates matter. From 9 April 2025 the UKGC capped online slot spin stakes at £5 for all adults. From 21 May 2025 it capped them at £2 for 18-to-24-year-olds specifically — justified by PGSI prevalence in that band, where 21.9 per cent score 1–27 and 5.3 per cent sit in the highest-risk 8–27 category.

The behavioural data the UKGC published from Q3 2025–26 onwards is the cleanest read on what the caps did. Sessions longer than an hour fell 16 per cent year-on-year, to 8.9 million across the quarter. Average session length dropped to 16 minutes. Total GGY rose despite the cap. The Market Impact Statement summarised it precisely: the data suggests the caps are not leading to a lack of activity or engagement with online slots games, but that the inability to place large stakes is leading to players being less inclined to play for longer periods of time. The cap did not stop play. It changed the shape of it.

REGULATION

The stake-cap rule applies to every game classified as a "slot" under the UKGC taxonomy. Bingo, casino table games and live dealer games are not in scope. The cap is enforced at the game engine, not at the operator account level — turbo-stake spending is not possible at a UKGC-licensed slot even on a large balance. Offshore games run no such engine-level constraint.

The migration story has two layers. The first is the small high-stake cohort the operator policy team described — players who had structured £25, £50, even £200 spins into their bankroll discipline. The second, larger in raw account count, is the marginal player who sees offshore sites in every Reddit thread and forum sidebar. The publicity around the cap did the convincing work for that cohort.

The £5 cap shrank long sessions by 16 per cent and average session length by two minutes. It did not shrink total GGY at the licensed market. It did, by the available evidence, accelerate offshore migration among the players for whom large-stake spinning was the product they wanted.

Bonus Architecture Outside UKGC: Wagering, Buys, Free Spins

Look at the bonus headlines on a non-GamStop landing page for a minute. Then look at the T&Cs linked from the footer. They tell different stories. The headline is the marketing surface. The T&Cs are the contract. The gap between them is wider in the offshore segment than anywhere else in the UK-facing gambling stack — by design, because the regulatory ceiling on wagering multipliers does not apply.

CONTEXT

From 19 December 2025 the UKGC capped bonus wagering at 10× the bonus amount. Before this rule, UKGC sites still ran wagering, but the median sat around 20–35×. The 10× cap is what reset the licensed market. Non-GamStop operators are not bound and have continued with the 35–45× range that was industry-standard before the cap.

Three structures dominate non-GamStop bonus marketing. The first is the welcome match — a percentage uplift on a first deposit, often 100 per cent to 200 per cent, with wagering applied either to the bonus alone or to bonus and deposit combined. The combined-wagering version is materially less favourable than the bonus-only version, and the offshore segment uses both. The second is the free-spins package. The third is reload and cashback mechanics targeted at existing accounts.

The mathematics is worth walking through. A £100 deposit, matched at 200 per cent for a £200 bonus, with 40× wagering on bonus, requires £8,000 of cycled wagering before winnings convert to withdrawable cash. A UKGC-licensed bonus capped at 10× wagering — £100 deposit, 100 per cent match for £100 bonus — requires £1,000. The offshore headline is bigger; the contract is eight times harder to clear. Game weighting compresses effective value further: slots typically count at 100 per cent, but the larger the bonus, the more likely the operator restricts the eligible catalogue. Bonus-buy features, not permitted on UKGC sites since 2023, are often explicitly excluded from bonus eligibility on offshore sites too.

Pragmatic Play occupied 9 of the 10 most-played slots across the broader UK-facing market in Q1 2025. The headline games in non-GamStop bonus offers are usually the same Pragmatic titles familiar from UKGC sites. The wrapper around them differs. The deconstruction of promotional structures at offshore venues is the dedicated topic of the next cluster.

Payment Rails at Non-GamStop Slot Sites

Payments are where the offshore market actually has to work hardest, and where its quoted speeds most often part company with reality. The UKGC benchmark for comparison is now extremely tight: 96.3 per cent of 44.2 million withdrawals on UKGC-licensed sites between June and September 2024 were processed automatically, 3.5 per cent within 24 hours, and only 0.1 per cent took more than 48 hours. The non-GamStop segment cannot replicate that profile uniformly. Some operators come close on crypto payouts; very few come close on fiat. UK card networks and bank rails do not directly support unlicensed operators, so the offshore segment routes through third-party processors that introduce a verification layer the licensed side does not need.

| Method | Deposit speed | Withdrawal speed | Effective fees | Notes |

|---|---|---|---|---|

| UK debit cards (Visa, Mastercard) | Instant | 2–5 working days | 0–3% spread on bank-side conversion if operator currency is EUR or USD | Some UK card issuers decline gambling-coded transactions to unlicensed operators outright. |

| E-wallets (Skrill, Neteller, MuchBetter) | Instant | Hours to 24 hours | 1–2.5% | Skrill and Neteller route through third-country licences; player needs to fund the wallet first. |

| Open Banking / pay by bank | Instant | 1–3 working days | Minimal | Less common at offshore venues; depends on provider–operator licence compatibility. |

| Bitcoin / Ethereum | 10 minutes to 1 hour | Same window | Network fee only | Operator typically holds in BTC or ETH; player carries volatility risk. |

| USDT / USDC stablecoins | Minutes | Minutes | Network fee only | Increasingly the default offshore payout rail; eliminates volatility but requires a wallet. |

| Apple Pay / Google Pay | Instant | Rare | Card-network rules apply | Limited because the underlying card may decline gambling MCC. |

5.8 per cent of UK gambling-site users now report routing access through a VPN, and the rate has climbed roughly 40 per cent above the pre-July-2025 baseline since the Online Safety Act took effect. The increase is not slot-specific — it spans all online gambling — but the slot segment carries the largest share of the migrating cohort.

The crypto rails are where the offshore segment has built its actual speed advantage. A USDT withdrawal that clears in minutes is genuinely faster than a UK bank-rail withdrawal from any operator on either side of the perimeter. The trade-offs are familiar: the player needs a wallet, seed-phrase security, and the FCA registration requirements that apply to UK-based crypto-asset firms but not to offshore operators receiving deposits. The architecture of payout channels including digital assets at non-GamStop venues is mapped in the dedicated cluster.

Fiat-side payouts are where "instant withdrawal" claims most often unravel. Actual processing depends on whether the operator's payment partner can clear to a UK account at all, whether KYC has been completed at the first request, and whether the withdrawal sits within daily or monthly caps. Quoted speeds tend to assume a fully verified account with no anti-fraud holds. Read them as ceilings, not averages.

Risks Outside UKGC: What Players Forfeit

This is the section the rest of the article was building toward. The legality question has a clean answer; the protection question does not. What a player gives up at the perimeter is rarely listed in full anywhere in the non-GamStop sector — for obvious commercial reasons.

Start with the affected population. 562,000 people are on GAMSTOP. The Ipsos study commissioned for GAMSTOP in 2024 found that 75 per cent of users had stopped playing online entirely; the remaining 25 per cent is the recidivism cohort that Yield Sec uses to estimate offshore losses. Run on 532,484 enrolled users at 25 per cent relapse, that prices potential losses to self-excluded players at £426 million a year. NHS England's Adult Psychiatric Morbidity Survey for 2023–24 reports 0.3 per cent of all English adults at the clinical problem-gambling threshold, rising to 0.9 per cent of those who gambled in the previous twelve months. In the 18–24 band, 5.3 per cent sit in the highest-risk PGSI 8–27 category.

RISK

"Protection layer" is not a marketing term. When a UKGC-side operator fails to pay out or applies an unfair contract term, the player has a defined route through the operator's Alternative Dispute Resolution body, with the UKGC as regulator of last resort. At a non-UKGC site, the equivalent route depends on which jurisdiction's regulator the operator is willing to engage with. Many do not engage at all. Tim Miller has described some non-GamStop sites in court testimony as sophisticated international criminal networks — phrasing from a coroner's hearing, not the regulator's marketing.

What stays in place when you stay UKGC-side

- GAMSTOP integration that enforces self-exclusion across every licensed operator.

- Mandatory dispute resolution through IBAS or another approved ADR body, with binding awards.

- Game-output auditing through accredited test houses; published RTP figures the operator must honour.

- Financial vulnerability triggers at defined thresholds, designed to catch escalating spend.

- 10× bonus wagering cap as a floor on bonus fairness.

What is at the operator's discretion offshore

- Whether a withdrawal is honoured in the timeframe quoted, or held pending discretionary review.

- Whether published RTP matches the version of the game actually loaded.

- Whether bonus T&Cs are revised mid-promotion without notice.

- Whether a self-exclusion request is honoured at sign-up.

- Whether dispute correspondence is answered at all.

The traffic-graph dimension is the one player-facing content usually skips. 89 per cent of UK views of illegal sports streaming content carried advertising for unlicensed gambling sites alongside malware, spyware or keylogger payloads. Not every non-GamStop operator buys that inventory, but the underlying dynamic, in Ismail Vali's framing, is that illegal online gambling in Great Britain is now knocking on the door of 10 per cent market share, achieved through the cynical exploitation of two vulnerable audiences — children and self-excluded gamblers on the GAMSTOP scheme. The dispute machinery is the part that matters most when something goes wrong, and a complete map of operator safety due diligence across the offshore segment is treated in its own guide.

A Methodology for Reviewing a Non-GamStop Slot Site

The framework I use to review a non-GamStop site has changed twice since I started in 2017 and stabilised in its current form around mid-2024. It is six checks, all verifiable without depositing, runnable in roughly thirty minutes. The output is not a recommendation — the framework refuses to recommend, by design. It is a filter that drops operators below a threshold of acceptability and leaves the rest for the player to decide between.

METHODOLOGY

The six checks: licence verifiability (is the licence number searchable on the issuing regulator's public register, and does it match the operator's trading name?); ownership chain (is the legal entity behind the brand identifiable and the same one named in the T&Cs?); bonus-clause integrity (do the T&Cs contradict the marketing page on max-cashout, wagering, game restriction and time window?); payout machinery (which payment partners are named and what are their published limits?); dispute mechanism (which ADR body, if any, does the operator name, and is it real and contactable?); software supply chain (which game studios are listed, and do those studios publicly acknowledge the operator as a partner?).

The first check filters more operators than any other. A licence reference that looks plausible — "Curaçao 8048/JAZ2020-098" or similar — does nothing for a player unless the issuing register confirms it. Curaçao now operates a public register under the new LOK regime; MGA's has been searchable for years; Anjouan's is patchier. If the operator names a licence and the issuing body has no record of it, that is the end of the assessment. The second check filters brands spun up under shell companies to absorb risk: if the T&C entity differs from the licence record and neither share register is accessible, the player has no counterparty to serve a complaint on.

Cross-reference with payout speeds. The UKGC benchmark of 96.3 per cent auto-processed withdrawals on licensed sites is the comparison number; an offshore operator quoting "instant withdrawals" should be matched against player-reported actual timings on third-party tracker forums, not the operator's own copy. Same for advertised RTP — the version that loads on the operator's domain is what the player actually plays; the version advertised is what the marketing team decided to print.

Do, in order

- Pull the licence number into the issuing regulator's public register and confirm an exact match on trading name.

- Read the bonus T&Cs in full before depositing — max-cashout, time window, max-bet during wagering, eligible games.

- Cross-check published payout speed against third-party player reports.

- Confirm the operator's named ADR body exists and accepts complaints in the player's residence.

Don't, regardless of marketing copy

- Treat licence imagery in the footer as proof of licence — only register confirmation counts.

- Deposit before the operator's first KYC request — front-loaded verification protects withdrawal speed later.

- Assume RTP shown on review sites matches the live game; check inside the paytable on the operator's own domain.

- Take silence on ADR as neutral — it is the single biggest indicator that a dispute will not be resolved.

This framework reduces the list of operators a UK player might consider from the public market of several hundred to a much smaller set of operators that fit specific player profiles on review. The cluster article behind that link walks through the matrix in operator-by-operator detail; the pillar concern here is only the method.

Enforcement Trajectory: UKGC Action & the 2026 Outlook

The first cease-and-desist letter I tracked from the UKGC in 2017 was a curiosity — a small enforcement unit firing at a tiny number of targets, mostly affiliates. Eight years later, that letter is one of more than 770 sent since April 2024, the criminal caseload has grown 300 per cent in a single year, and a cross-departmental taskforce sits above the regulator with a mandate that reaches the payment rails.

The numbers tell the trajectory plainly. From April 2024 to early August, the UKGC issued 344 cease-and-desist notices, reported 45,674 URLs to search engines, secured the removal of 30,605, pushed 466 sites to delisting and got 235 disconnected or geo-blocked outright. By ICE Barcelona in early 2026, Andrew Rhodes was citing more than 770 cease-and-desist letters in total — 262 to operators, 205 to advertisers — and 64,000 URLs removed by Google. The criminal-case curve climbs in parallel: "Year on year we saw a 300 per cent increase in the number of criminal cases we were taking as a regulator," Rhodes told the IAGR keynote in Toronto.

What changed in May 2026 reframes the previous eight years. On 14 May, DCMS published the charter of the Illegal Gambling Taskforce, with three priorities: blocking payments to unlicensed operators, attacking their advertising, and forcing inter-agency coordination across the Commission, HMRC, the National Crime Agency and the major payment networks. The first is the operational one — cease-and-desist letters travel slowly; payment-channel disruption arrives the same day.

REGULATION

From April 2026, Remote Gaming Duty rises to 40 per cent. The increase falls on UKGC-licensed operators directly; the indirect effect is that UK-licensed margins contract while the Commission's enforcement budget has to expand into a wider target list. Players should expect more rapid payment-channel blocks, faster ISP-level interventions, and increasing reach into the platforms Tim Miller named at ICE Barcelona 2026: "Anyone who spends time on their platforms will likely have seen ads appearing for illegal online casinos."

Player behaviour is already responding. Since the Online Safety Act took full effect in July 2025, the Commission's Data Innovation Hub has recorded a stable VPN-usage increase of roughly 40 per cent above the pre-OSA baseline. The direction of travel for the rest of 2026 is unambiguous: enforcement volume rises, payment-channel pressure becomes the dominant lever, and the offshore market adjusts to a regulator that has stopped treating it as peripheral.

Frequently Asked Questions

What exactly are non-GamStop slots and how do they differ from UKGC-licensed slots?

Non-GamStop slots are reel games hosted by operators that hold no UK Gambling Commission licence and are therefore not connected to the national self-exclusion register. The games themselves are often the same titles found at UKGC sites, but the operator wrapper differs: licensing is offshore, KYC is later, statutory stake caps do not apply, and disputes run through the offshore regulator rather than IBAS.

Is it legal for a UK resident to play at a slot site that is not on GamStop?

Playing is not a criminal offence under UK law. The Gambling Act 2005 makes operating without a UK licence the illegal act, and that liability sits with the operator, not the player. A UK resident depositing at an offshore site is acting lawfully but is outside the consumer-protection framework the UKGC enforces. Lawful and protected are not the same word.

Which licences do non-GamStop slot operators actually hold, and how reliable are they?

Four regimes account for almost the entire offshore market visible to UK players: Malta Gaming Authority, Isle of Man, Curaçao and Anjouan. Curaçao is the largest by population and the most relevant in 2026: all sub-licences under the old master-licence system were voided on 31 January 2025, so any operator still advertising a pre-LOK sub-licence is operating on documentation that no longer exists.

Master-licence — under the pre-LOK Curaçao framework, four master-licence holders could issue sub-licences to operators, with no direct regulator relationship to the operating company; LOK abolished this structure.

How do the £5 and £2 stake caps affect the choice between UKGC and offshore slot sites?

The caps are the single largest structural difference between the two markets in 2026. Since 9 April 2025 every adult at a UKGC site is held to £5 per spin; since 21 May 2025 players aged 18 to 24 face £2. Offshore sites apply no equivalent ceiling. For high-volatility play this is the principal pull factor toward offshore venues.

What payment methods and withdrawal timeframes apply at non-GamStop slot sites?

Deposit channels are broader than at UKGC venues: debit and credit cards, cryptocurrencies including Bitcoin and stablecoins, e-wallets, prepaid vouchers and direct bank transfer. Crypto clears in minutes to hours, e-wallets in hours to a day, card and bank in two to five working days. Any operator quoting "instant" should be matched against player-reported timings rather than marketing copy.

Which slot providers are typically available at non-GamStop sites that UKGC restricts?

Two categories matter. The first is studios supplying both markets but shipping different configurations — Pragmatic Play, Hacksaw Gaming, Push Gaming, Nolimit City and Relax Gaming distribute to UKGC and offshore venues, but offshore versions retain bonus-buy features, configurable RTPs below 94 per cent and higher max-win multipliers. The second is studios that have withdrawn from the UKGC market entirely after the 2025 reforms.

What protections does a player lose by leaving the GamStop perimeter?

GamStop self-exclusion stops working — and 75 per cent of GamStop users, the 2024 Ipsos figure, stay away from online gambling because that perimeter holds. Statutory deposit limits and the £5 and £2 caps no longer apply. Financial risk assessments are absent. Reality checks are discretionary. Complaints cannot be escalated to IBAS or the Financial Ombudsman Service, and refund routes through offshore regulators run in months rather than weeks.

Recommend

Written by the editors at non Gamstop slots UK.